Bridging Fiat and Digital Assets in Georgia (2026 Update)

Georgia remains one of the most workable jurisdictions in the region for bridging digital assets and local banking infrastructure. Transfers settle. Banks function. Platforms operate within a defined regulatory perimeter.

What has changed is not access — but structure. Two things stood out in recent testing: (1) onboarding has become heavier, and (2) certain USDT purchase routes can price far from a 1:1 benchmark.

MyCoins: When Compliance Becomes Operational Friction

The onboarding experience with MyCoins has materially changed. What previously felt procedural now feels investigative.

During our most recent verification cycle, the process extended well beyond identity confirmation. We were required to provide source-of-funds documentation and clarify transaction history dating back to 2018. The exchange involved multiple rounds of requests, re-submissions, and follow-up explanations.

In total, the process consumed more than six hours of active engagement. For a regulated platform, due diligence is expected. However, the depth and repetition of the documentation requests introduced significant operational friction.

For expats managing cross-border capital histories, this level of review transforms onboarding from a compliance formality into a time-intensive audit-style exercise.

Something has clearly shifted in internal compliance posture. Whether driven by banking relationships, regulatory alignment, or internal policy, the practical result is a heavier, more intrusive KYC experience than many users may anticipate.

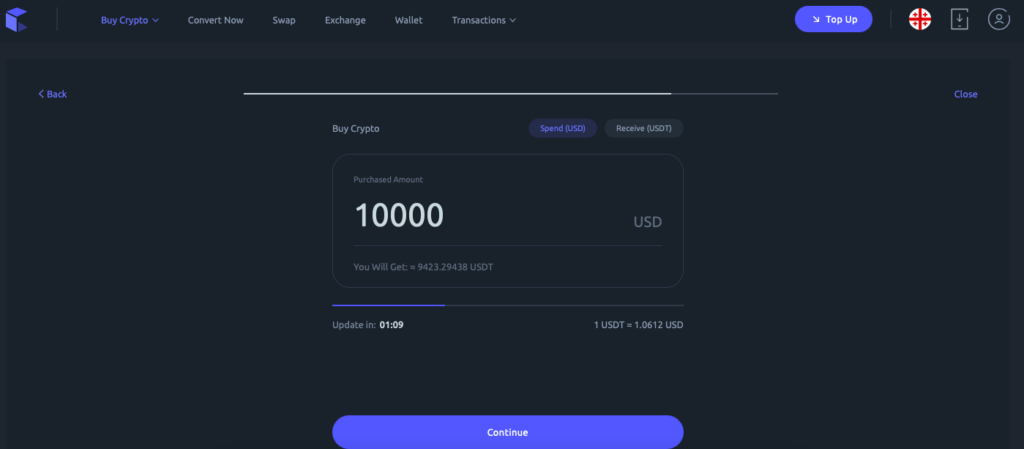

Cryptal: When “USDT” Stops Feeling 1:1

Cryptal’s product is clean and professional. The issue we observed is pricing on certain purchase routes — especially when buying USDT. For a stablecoin, the expectation is near 1:1 behavior relative to USD. In our testing, the quoted rate materially diverged.

We tested both card-based purchase and wire-funded flows. While there may be other execution paths, the routes we used produced pricing that, in practice, embeds a large execution premium.

This premium is not presented as a single “fee” line item. It is embedded in the quoted rate and can reflect a combination of spread, liquidity depth, payment-rail costs, and route-specific pricing. The practical point is simple: on a stablecoin, a ~6% divergence is economically significant.

For small amounts, the impact can be easy to overlook. At scale, it becomes a structural cost. If your goal is repeated conversions or treasury-style usage, this pricing makes the “easy button” hard to justify.

Forward Look

None of this should be read as “Georgia turning hostile.” The more plausible interpretation is institutionalization: tighter onboarding and more segmented pricing between convenience routes and cost-efficient routes. For expats, the adjustment is mindset: plan documentation, and treat execution path selection as part of the cost.

Figure 1 — Observed USDT Pricing Quote (February 2026)

Displayed rate: 1 USDT = 1.0612 USD at time of capture.